Considering a home on the fairway in La Quinta but unsure how to finance it? If you are exploring a second home in a country‑club community, you are likely hearing the term “jumbo loan.” The rules feel different because they are. In this guide, you will learn how jumbo loans work for second homes in La Quinta, what lenders review, how appraisals treat golf and club properties, and the steps to prepare a strong file. Let’s dive in.

Jumbo basics in La Quinta

A jumbo loan is any mortgage amount that exceeds the Federal Housing Finance Agency’s conforming loan limit for the county. These loans are not purchased by Fannie Mae or Freddie Mac and are held or sold by private lenders. That is why requirements can be stricter and more detailed.

For 2024, the baseline conforming limit for a one‑unit home in most counties is $766,550. If your La Quinta loan amount is above the county’s conforming limit, it will be treated as a jumbo loan with lender‑specific pricing and underwriting. This matters in La Quinta because many golf and resort properties sit in higher price tiers.

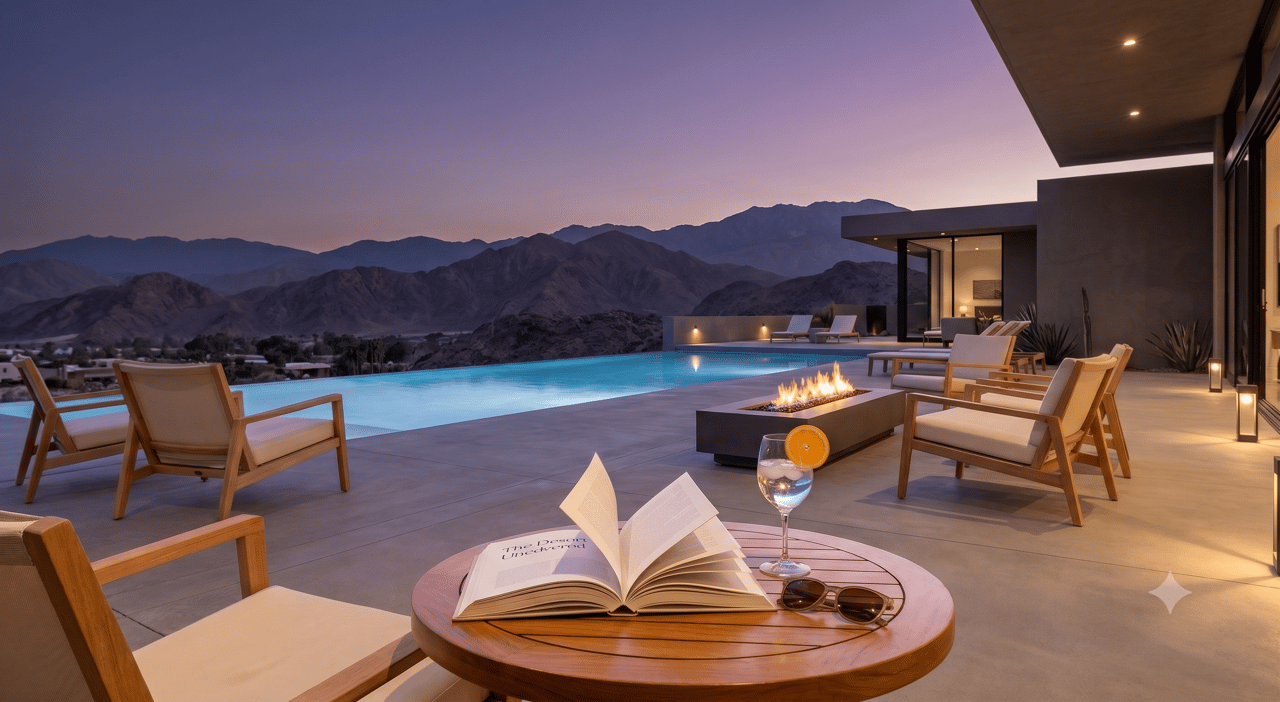

Why resort properties often require jumbos

La Quinta is a desert resort market with many gated communities, golf course frontage homes, and luxury custom estates. Prices in these neighborhoods frequently exceed conforming limits, which triggers jumbo financing for many second‑home buyers.

High‑end properties can also be unique. Custom architecture, view lots, and significant outdoor living upgrades make it harder to find recent, similar sales. That can increase appraisal scrutiny compared with standard suburban homes.

How lenders underwrite second‑home jumbos

Lenders review second‑home loans carefully, and more so when the loan is jumbo and the property is a resort‑style home.

Credit and debt ratio

- Strong credit matters. Many jumbo programs favor mid‑700s credit scores for best pricing and approval. Lower scores can still work but may require a larger down payment or higher costs.

- Debt‑to‑income ratio is key. While some conventional programs allow ratios up to about 43 to 50 percent with strong compensating factors, jumbo and second‑home loans often target lower ratios, especially at higher loan amounts.

Down payment and reserves

- Expect larger down payments than on conforming loans. A common range for jumbo second homes is 20 to 30 percent down, depending on your profile, loan size, and property type.

- Cash reserves are a frequent requirement. Many lenders want 6 to 12 months of principal, interest, taxes, and insurance left in liquid assets after closing for jumbo second homes.

Income and documentation

- Full documentation is the norm. You should plan to provide W‑2s or tax returns, recent pay stubs, and 2 to 3 months of bank and investment statements.

- Source and paper‑trail all funds. Large deposits and gift funds need clear documentation.

Occupancy and rental plans

- Second home means you will use the property part of the year and not operate it primarily as a rental. Lenders usually require an occupancy declaration.

- Investment property rules apply if you plan to run short‑term rentals through platforms or use the home primarily for rental income. Investment loans have different pricing, higher reserve and down payment needs, and different qualifying rules.

- Hybrid use varies by lender. Some allow limited rental; others classify any short‑term rental plan as investment use. Your HOA and city rules can also dictate what is allowed.

HOA and club fees

- Lenders review HOA documents, budgets, reserve funding, and any pending litigation. Higher HOA dues or special assessments affect your qualifying ratios.

- Country‑club memberships and dues may not be part of the mortgage payment, but they are real monthly costs. Lenders often ask for documentation to confirm overall affordability.

Property type specifics

- Condos and PUDs can require project reviews that look at owner‑occupancy levels, reserves, and litigation. Resort‑linked projects can face extra scrutiny.

- Detached homes in country‑club communities are usually underwritten as standard single‑family homes, but lenders still examine unique features and valuation.

Appraisals for La Quinta golf and club homes

Jumbo lenders typically require a full interior appraisal by an appraiser who understands the local luxury market. At higher loan amounts, some lenders require two appraisals or a second‑level review.

Comparable sales are scarce at the top

Luxury properties can be one‑of‑a‑kind, so truly comparable sales may be limited. Appraisers must justify time adjustments, market area boundaries, and any price differences with care. In some cases, sales from nearby cities like Palm Desert, Indian Wells, or Rancho Mirage may be used if La Quinta comps are too sparse, with a clear explanation of why those markets are comparable.

Golf frontage and views

Direct golf course frontage or premium views can add value if the data supports it. Appraisers look for recent sales with similar frontage and view orientation to quantify any premium. Unsupported or generalized “view” premiums are likely to be challenged by lenders.

Amenities and community differences

Country‑club amenities can matter. Private golf access, clubhouse services, pools, tennis or pickleball, and security may influence value, but only when comparable sales show similar amenities. Appraisers align the subject property with comps that mirror the same amenity level.

Interior finishes and custom upgrades

High‑end finishes and recent renovations can move value when they are well documented. Provide itemized lists, invoices, builder contracts, and photos for major upgrades like kitchen overhauls, custom flooring, and integrated smart‑home systems. Clear documentation helps the appraiser support adjustments.

Lot, privacy, and outdoor living

Lot size, privacy, orientation, landscaping, and outdoor kitchens all play a role. Water features and extensive hardscaping should be supported by market evidence showing buyers pay for those elements. The more precise your documentation, the easier it is for an appraiser to make quality adjustments.

Condition and systems

Mechanicals matter. HVAC, pool equipment, roof condition, and major systems affect lender risk. If issues emerge, a lender may require repairs or escrows prior to closing. Most La Quinta homes connect to municipal water and sewer, but verify each property’s setup.

Seasonality and timing

La Quinta’s seasonal demand can shift quickly. Appraisers explain seasonality and time adjustments when comps span different months or market phases. Older high‑end comps can be used when recent sales are limited, with careful justification.

Short‑term rental influence

Most appraisals value the home as a residence, even if short‑term rentals are common in the area. If a property is marketed for short‑term rental use, some lenders may review rental documentation, but arm’s‑length residential sales are still the primary valuation anchor. How your lender classifies occupancy will drive loan terms.

Insurance and hazard factors

Flood zones, earthquake exposure, and wildfire risk can affect insurability and cost. Lenders will require proof of acceptable insurance coverage, and appraisers note these factors in the report.

Cost planning for La Quinta second homes

Plan for the full monthly picture. In addition to principal and interest, budget for property taxes, HOA dues, insurance, and any country‑club dues or assessments. Some communities have special assessments. Lenders will include these expenses in your qualifying analysis and reserve requirements.

If membership is required, confirm what is mandatory and what is optional. Club fees are not part of your mortgage payment, but they are an ongoing expense and must fit your budget.

Your preparation checklist

Use this practical list to prepare a smooth jumbo second‑home purchase:

Documentation and funds

- Gather 2 or more years of tax returns, recent pay stubs, and 2 to 3 months of bank and investment statements.

- Paper‑trail large deposits and gift funds with clear letters and statements.

- Confirm down payment funds and estimate post‑closing reserves. Target 6 to 12 months of PITI for jumbo second homes, subject to lender rules.

HOA, club, and rental rules

- Obtain the HOA packet early, including CC&Rs, budget, reserve study, meeting minutes, and litigation disclosures.

- Confirm whether club membership is required and outline all dues and fees that will affect your monthly budget.

- Review community and local rules on rentals, especially short‑term rentals, to understand how your use plan may affect loan type.

Appraisal readiness

- If selling, compile an upgrade list with invoices and photos and address safety or system issues early.

- If buying, work with a lender and agent who use appraisers experienced in Coachella Valley luxury properties.

Insurance, taxes, and assessments

- Request insurance quotes early for hazard and any specialty coverage you need.

- Verify tax rates and any special assessments. Plan for potential supplemental tax bills after purchase.

Lender selection

- Choose a lender with active jumbo programs and local resort‑property experience.

- Ask about minimum credit scores, maximum DTI, reserve requirements, condo or project approvals, and whether a second appraisal could be required at your price point.

If short‑term rentals are part of your plan

- Verify local ordinances and HOA restrictions before you make offers.

- Discuss with your lender how rental intent will affect occupancy classification and whether documented rental income can be used to qualify under investment guidelines.

How a trusted advisor adds value

The right representation protects your interests and smooths a complex process. A La Quinta second‑home purchase often involves HOA rules, club membership details, and appraisal nuances tied to golf frontage, views, and custom features. You benefit when your advisor understands these layers and aligns your offer strategy with lender expectations.

With attorney‑level contract insight and deep knowledge of country‑club communities, you can structure clean contingencies, request the right HOA and club disclosures, and anticipate lender and appraisal milestones. That level of preparation helps you move confidently and keep timelines on track.

Next steps

- Get prequalified early with a lender that regularly funds jumbo second‑home loans in La Quinta. Ask about down payment, reserves, and appraisal expectations.

- Verify HOA documents, club obligations, rental rules, insurance quotes, and tax details for each property you consider.

- Align your offer strategy with likely loan terms, and be ready with documentation the moment you write.

If you want a clear path from search to closing across La Quinta’s country‑club and gated communities, connect with a local advisor who blends luxury market knowledge with contract precision. Work with Kimberly Oleson to explore the right neighborhoods, navigate HOA and club requirements, and position your jumbo second‑home purchase for success.

FAQs

What is a jumbo loan for a La Quinta second home?

- It is a mortgage amount above the county’s conforming loan limit, making it ineligible for Fannie Mae or Freddie Mac and subject to private jumbo underwriting.

How much down payment do jumbo second homes typically require?

- Many programs ask for 20 to 30 percent down, with stronger profiles sometimes qualifying for the lower end of that range.

What credit score do lenders prefer for jumbo second homes?

- Lenders often look for mid‑700s credit scores for best pricing and approval, with lower scores requiring stronger compensating factors.

How many months of reserves should I plan for?

- A common expectation is 6 to 12 months of PITI in liquid assets after closing, depending on the lender, loan size, and your profile.

Can I use short‑term rentals and still call it a second home?

- If your primary intent is rental income, lenders usually classify the property as an investment, which changes pricing and requirements; limited rental policies vary by lender and HOA rules.

Do HOA dues and club fees affect my loan approval?

- Yes, lenders factor HOA dues and special assessments into qualifying ratios, and they may review club fee obligations as ongoing household expenses.

Why are appraisals for golf properties more complex?

- Unique features, view premiums, and limited comparable sales make supportable adjustments harder, so lenders and appraisers scrutinize these reports closely.

Could a lender require two appraisals on a high‑value home?

- Some lenders order a second appraisal or a review for higher loan amounts to validate value and manage risk.